- The Deal Brief - Insurance

- Posts

- Insurance 150 x CapLink Launches | $3.7B Deal, CA Auto Breakdown, and NYC Summit Revealed

Insurance 150 x CapLink Launches | $3.7B Deal, CA Auto Breakdown, and NYC Summit Revealed

It’s Wednesday and we’re diving into the breakdown of California’s auto insurance market.

In partnership with

Hi ,

This Wednesday we’re excited to announce a strategic partnership between Insurance 150 and CapLink Group, combining two trusted forces in B2B media and events.

Together, we’re launching Insurance 150 x CapLink Group—a unified platform for investors and executives in the broad Insurance/FIG industry who want to access the heart of it’s ecosystem.

From live summits and bespoke research, precision-targeted newsletter advertising to 400,000 investors and executives every week, we now offer a complete, high-conversion media stack to help you grow your presence in this sector.

Check out our first collaboration here and watch out for Insurance/FIG events soon!

In our regular scheduled publishing, we’re diving into the breakdown of California’s auto insurance market, a $3.7B megamerger that could reshape UK insurance, and why Auto InsurTech has experienced exponential growth over the past decade.

Want to reach 350,000+ executive readers? Start Here.

Know someone who would love this? Pass it along—they’ll thank you later. Here’s the link.

DATA DIVE

When 13 Million Cars Become a Problem

California's auto insurance machine is breaking down. The state leads the U.S. with 13.1 million registered vehicles, but it’s also ground zero for regulatory and claims pressure. Liability and physical damage lines account for nearly 40% of all premiums—but are now the biggest loss-makers, thanks to soaring repair costs, litigation spikes, and rate lag. As more carriers pull out of high-risk ZIP codes, affordability gaps widen, pushing drivers toward the Low Cost Auto Insurance Program. For incumbents, 2026 might be the year where insurtech, AI, and rate flexibility decide who survives the squeeze.

TREND OF THE WEEK

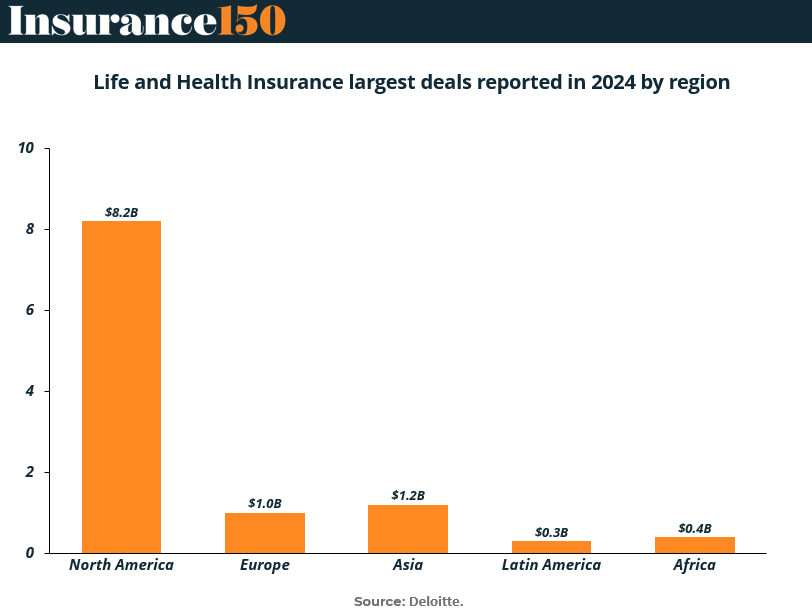

Headline North America Dominates 2024 Life & Health Insurance Mega-Deals

If you're hunting for blockbuster insurance transactions in 2024, look west. North America recorded $8.2B in the largest reported life and health insurance deals—more than 6x the combined total of Europe, Asia, Latin America, and Africa.

The global picture tells a story of capital asymmetry:

Asia: $1.2B

Europe: $1.0B

Africa + LatAm: $0.7B combined

The disparity reflects deep M&A pipelines in the U.S., capital recycling from private equity portfolios, and continued legacy block transactions—especially in the annuity space.

Why it matters: While emerging markets offer growth, North America is where scale, capital, and balance sheet transformation converge. For investors, this is where the deal flow is—until regulatory or macro shifts unlock volume elsewhere. (More)

PRESENTED BY MONEY

Outsmart college costs

Ready for next semester? June is a key time to assess how you’ll cover college costs. And considering federal aid often isn’t enough, you might have to consider private student loans.

You’re just in time, though—most schools recommend applying about two months before tuition is due. By now, colleges start sending final cost-of-attendance letters, revealing how much you’ll need to bridge the gap.

Understanding your options now can help ensure you’re prepared and avoid last-minute stress. View Money’s best student loans list to find lenders with low rates and easy online application.

MARKET MOVERS

Company (Ticker) | Last Price | 5D |

UnitedHealth Group Incorporated (UNH) | $ 301.90 | -1.85% |

Ping An Insurance (Group), (2318. HK) | $ 6.36 | 4.50% |

Elevance Health (ELV) | $ 374.23 | -0.61% |

Chubb Limited (CB) | $ 287.46 | 0.36% |

Allianz SE (ALV. DE) | $ 340.70 | 0.56% |

INSURTECH CORNER

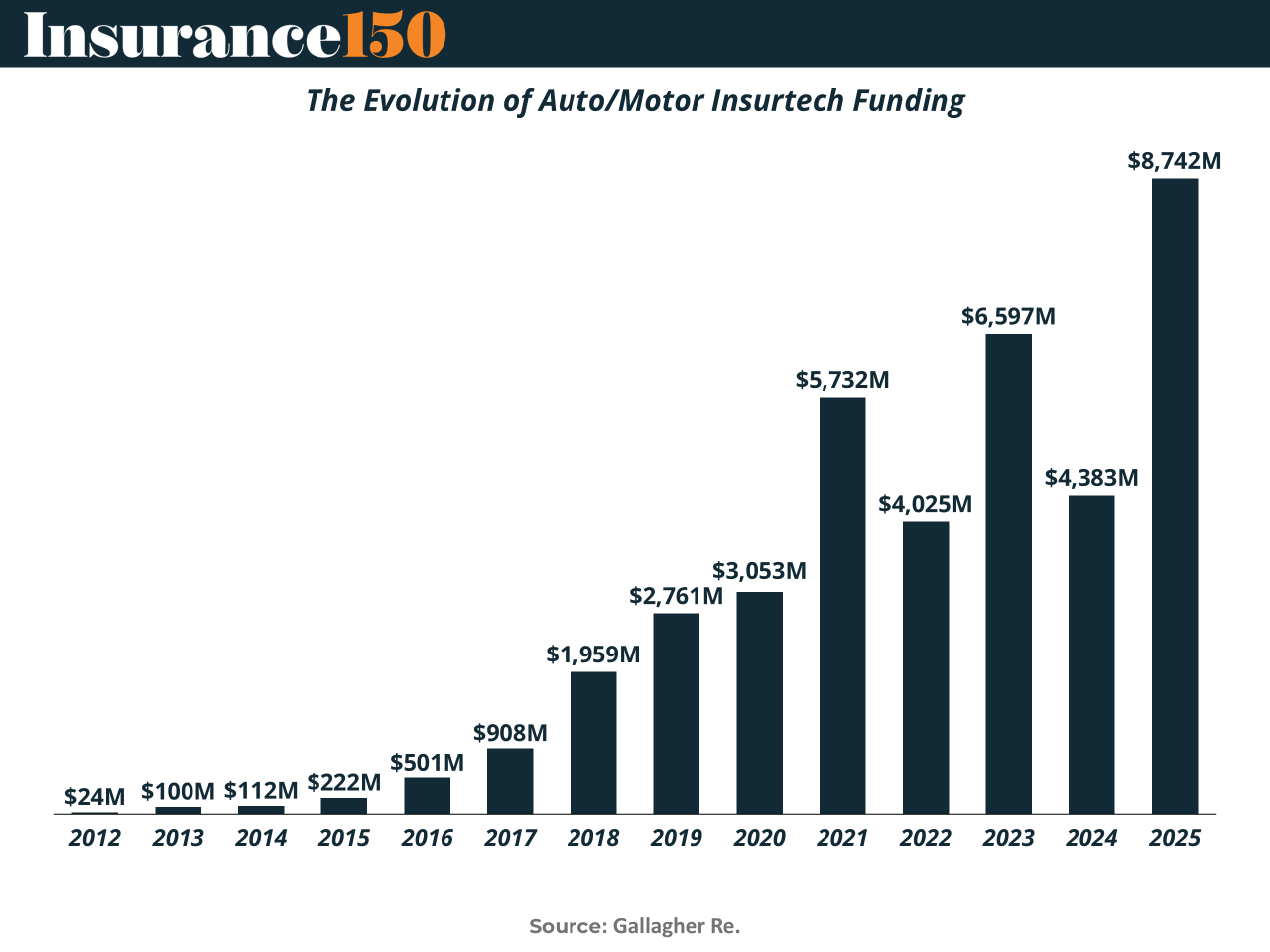

Auto InsurTech: From Garage to Growth Rocket

In 2012, Auto InsurTech barely registered, with just $24M in global investment. Fast forward to 2025, and we’re looking at a projected $8.7B—a nearly 400x increase. What changed? A structural inflection point in 2020–2021, where pandemic tailwinds and digital urgency nearly doubled funding overnight. Since then, we’ve seen capital flow into AI claims automation (Tractable), emerging market platforms (CarDekho), and geolocation/telematics infrastructure (Mapbox). The Zebra and Carrot Insurance only further highlight that this isn’t hype—it’s infrastructure-level capital backing the next mobility ecosystem. As global insurers rewire for mobility, Auto InsurTech is no longer a sideshow. It’s the main event. (More)

DEAL OF THE WEEK

Aviva Builds a Giant

Aviva’s £3.7B takeover of Direct Line Group has been blessed by UK regulators. The FCA and PRA greenlit the deal, while the SRA nodded at Aviva’s material interest in DLG Legal Services. What’s left? A High Court stamp of approval on July 1 and a CMA nod shortly after. Interestingly, Aviva waived the CMA clearance as a formal condition, betting on smooth sailing through competition review. Assuming that plays out, this merger will form a dominant player in UK insurance, marrying Aviva’s broad platform with Direct Line’s brand and distribution. A rare, full-stack consolidation play with clear strategic rationale—and regulatory backing. (More)

The Private Markets Intelligence Summit of the Year

📍 October 15, 2025 | Well& by Durst, NYC

Join 300+ private markets leaders—GPs, LPs, operating partners, and advisors—for a single day of insights, strategy, and dealmaking at the New York Private Capital Summit.

This isn’t another networking event. It’s where strategy meets substance:

→ Keynotes from HarbourVest, Bloomberg, Australian Super

→ Deep-dives on secondaries, direct lending, GenAI, and ESG

→ Practical panels on fund formation, human capital, and tax strategy

→ A spotlight on emerging liquidity tools and NAV-based financing

With over 50 senior speakers from firms like Apollo, KKR, Carlyle, Neuberger Berman, and Warburg Pincus, the Summit is designed for decision-makers driving the next decade of private capital.

Reserve your seat before it sells out: Early Bird Access

MACROECONOMICS

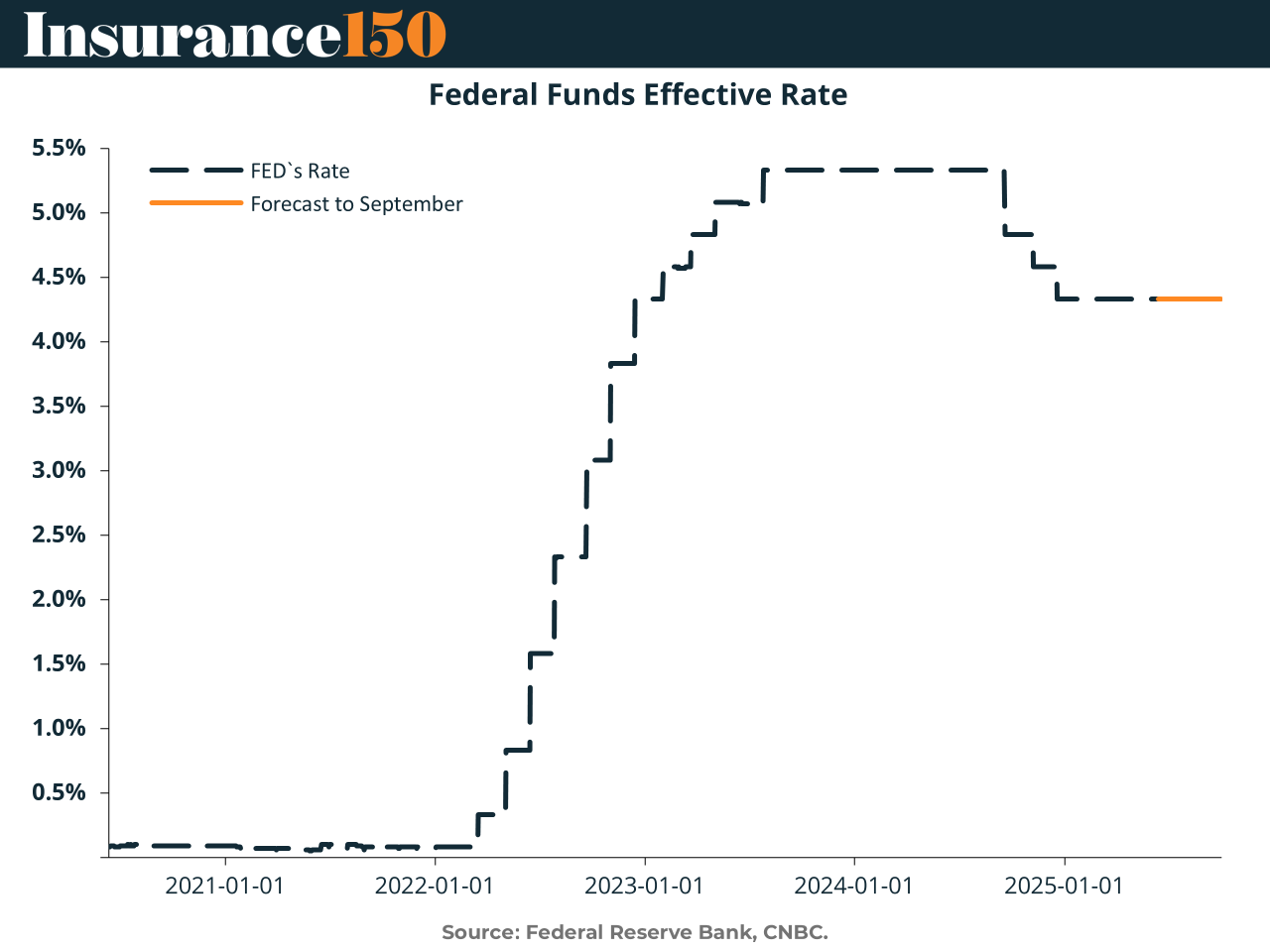

The Fed’s Waiting Game: Blame Trade, Not the CPI

Forget the soft CPI print—tariffs are the new inflation wildcard. The Fed is keeping rates pinned while it watches whether Trump-era trade skirmishes evolve into a cost spiral. Goods with elastic demand are shielding consumers—for now. But once pre-tariff inventories deplete, that buffer’s gone. The result: no policy loosening until trade talks settle. PE dealmakers should watch rate outlooks like they would a volatile GPAC partner—calm on the surface, chaos just beneath. No cuts till September at the earliest, and even that’s conditional. Inflation may be low, but uncertainty is still running hot. (More)

TWEET OF THE WEEK

@JonathanJLevin@Claudia_Sahm@conorsen The Fed left interest rates unchanged and continued to pencil in two rate cuts in 2025, saying uncertainty over the economic outlook was still high but had diminished.

🎥 @JonathanJLevin joined @Claudia_Sahm and @conorsen LIVE to discuss

— Bloomberg Opinion (@opinion)

6:25 PM • Jun 18, 2025

"The future belongs to those who believes in the beuty of their dreams"

Eleanor Roosevelt